The Legacy Liquidation Trap

- Michael Jesse

- Jan 30

- 11 min read

Long-Term Care Financial Planning to Stop the Ignorance Surcharge

As a Household CFO, you’ve spent decades mastering the art of the "Earn." You’ve optimized your portfolio, hedged against volatility, and protected your downside. But now, you are entering a new, predatory arena: The Long-Term Care Racket.

The system isn't just "complex"—it is a high-speed wealth-extraction engine. It banks on your exhaustion, your grief, and your lack of a law degree. Every day you spend "trying to figure out" the difference between Medicare and Medicaid is a day the system levies an Ignorance Surcharge against your parent’s estate.

At 2nd Look Services, we don't just offer "advice." We provide a Financial Equalizer. We use AI-driven Forensic Reviews of Long-Term Care Laws to out-read the bureaucrats and ensure you Earn, Return, and Retain every cent of your family’s legacy.

The Forensic Sweep: Auditing the Three Pillars of Systematic Loss

To stop the bleed, you must move beyond merely relying on "hope" and instead transition into a proactive and structured approach known as Forensic Governance.

This concept emphasizes the importance of meticulous scrutiny and accountability in managing resources, particularly when it comes to safeguarding your family’s financial well-being. It is imperative to recognize that in order to effectively secure and preserve your family’s capital, you must engage in a comprehensive audit of the three key professions that currently serve as gatekeepers to your financial assets.

Understanding Forensic Governance

Forensic Governance involves a rigorous examination of the systems, practices, and individuals that oversee your financial resources. This approach not only seeks to identify potential inefficiencies or risks but also aims to enhance transparency and trust in the management of your capital. By moving into this realm, you are taking a decisive step towards ensuring that your family's financial future is not left to chance or blind faith.

The Role of Gatekeepers

The three professions that typically act as gatekeepers to your family’s capital include financial advisors, accountants, and attorneys. Each of these roles plays a crucial part in the management and protection of your assets, but they must be held accountable to ensure they are acting in your best interest.

Financial Advisors

Financial advisors are responsible for guiding investment decisions and helping families navigate the complexities of financial markets. However, it is essential to scrutinize their qualifications, fee structures, and the underlying motivations behind their recommendations. An audit of their performance and adherence to fiduciary standards can reveal whether they are truly prioritizing your family's financial health or merely pursuing their own interests.

Accountants play a vital role in managing tax obligations and ensuring compliance with financial regulations. Their expertise can significantly affect your family’s capital through strategic tax planning and financial reporting. However, it is crucial to evaluate their methodologies and the accuracy of their work. An audit of their practices can uncover potential areas for improvement, such as optimizing tax strategies or identifying overlooked deductions that may benefit your family financially.

Attorneys

Attorneys are key players in the realm of estate planning and legal protection of your family’s assets. They help draft wills, trusts, and other legal documents that secure your family's legacy. However, not all attorneys are created equal, and their effectiveness can vary widely. An audit of their services should focus on their understanding of your family’s unique circumstances and their ability to adapt legal strategies to meet your evolving needs.

The Importance of Accountability

By conducting a thorough audit of these three professions, you are not only protecting your family’s capital but also fostering a culture of accountability and transparency.

This process will empower you to make informed decisions and take control of your financial future. It is essential to establish regular check-ins and reviews with these gatekeepers to ensure that they remain aligned with your family's goals and values. In conclusion, moving beyond hope into Forensic Governance is a critical step in safeguarding your family’s financial capital. By auditing the financial advisors, accountants, and attorneys who serve as gatekeepers, you can ensure that your family's resources are managed effectively and ethically. This proactive approach will provide you with the peace of mind that comes from knowing your capital is in capable hands, ultimately allowing your family to thrive and prosper.

The Financial Pillar: Combatting the "Asset Stripping" Engine

This is where the "Riled Up Visionary" meets "Growth Engineering." We aren't just talking about a budget; we are talking about a Systemic Wealth Extraction Engine. The long-term care industry is designed to liquidate a senior’s life work before providing a single cent of subsidy.

If you are a Household CFO "Self-Funding" without a forensic strategy, you are losing an average of $12,000 to $18,000 per month. That isn't an expense; it’s an unforced error. Here is the technical breakdown of how the Ignorance Surcharge is siphoning your family's capital.

1. The Medicaid "Look-Back" Ambush: Weaponized Auditing

The state doesn't just look at what your parents have today; it performs a Forensic Audit of every check written for the last 60 months.

The Trap: If your parent gave a grandchild $10,000 for college four years ago, the state doesn't see a "gift"—they see an "uncompensated transfer." They will apply a Divestment Penalty Divisor (the average monthly cost of nursing care in your state).

The Math of Loss: If your state’s divisor is $10,000, that one $10,000 gift triggers a one-month penalty period where Medicaid pays $0. You just paid a $10,000 Ignorance Surcharge because you didn't utilize a Caregiver Contract or a Medicaid Compliant Annuity.

The Forensic Solution: We use AI to identify these "transfers" before the state does. We help you implement Life Care Agreements—legal contracts that turn "gifts" into "payments for services," allowing you to legally spend down assets while keeping the capital within the family ecosystem.

2. The VA "Aid & Attendance" Invisible Pension: The 40-Page Gauntlet

There is a tax-free pension worth over $2,500/month ($30,000+ per year) available to wartime veterans and their surviving spouses. Yet, 60% of eligible seniors never receive it.

The Barrier: The application is a 40-page bureaucratic gauntlet designed to trigger an automatic denial if a single box is checked incorrectly. The VA looks at your "Net Worth" (capped at $163,699 in 2026), but they allow you to deduct Unreimbursed Medical Expenses (UMEs).

The Cost of Delay: Most families wait until the crisis hits to apply. Because the VA takes 6–12 months to process a claim, and they do not always pay retroactively to the date of the need, you can lose $30,000 in unrecoverable benefits while waiting for a caseworker to answer the phone.

The Growth Strategy: We don't "wait for the crisis." Our Forensic Sweep identifies veteran status immediately, ensuring the application is engineered for approval on the first pass, reclaiming thousands in monthly cash flow.

3. The Homestead Loophole: Protecting the Primary Residence

The greatest fear of any Household CFO is losing the family home to the state.

The Racket: Nursing homes will often pressure families to sell the home to pay for care. They won't tell you that in many states, the home is an Exempt Asset (up to certain equity limits) as long as there is an "intent to return home" or a spouse living there.

The Failure: Without a Forensic Review, families sell the house, pay the facility, and then apply for Medicaid—meaning they just "gifted" the facility $300,000 of equity that could have been protected for the heirs.

The Household CFO's Financial Audit

Asset Category | The "Default" Loss | The 2nd Look Recovery |

Cash Savings | 100% liquidated to $2,000 limit. | Converted to Medicaid Compliant Annuities to provide income for the healthy spouse. |

Family Home | Forced sale to pay private rates. | Life Estate or MAPT implementation to protect equity from estate recovery. |

Veteran Status | Ignored; paying $12k/mo out-of-pocket. | $2,874/mo (Married Vet) cash infusion to offset assisted living costs. |

The Legal Pillar: Solving the "Admin Rights" Crisis

To a Household CFO, "Admin Access" is everything. You wouldn't run a corporation where the CFO is locked out of the treasury, yet millions of children of seniors are operating under a legal illusion. You believe that because you have a signed Power of Attorney (POA) in a desk drawer, you have control.

You don't.

In the eyes of the state and financial institutions, a flawed POA is just a piece of paper. If the legal "code" is wrong, the system crashes the moment a crisis hits, triggering a massive Ignorance Surcharge in the form of frozen assets and court-ordered guardianship. Here is the deep-dive forensic audit of the legal chokepoints designed to strip you of your authority.

1. The "Durable" vs. "Springing" Fatal Flaw

Most estate planners of the last generation used Springing Power of Attorney. On the surface, it sounds logical: it only "springs" into action when the parent is incapacitated. In practice, it is a catastrophic administrative bottleneck.

The Bureaucratic Delay: To activate a Springing POA, you typically need two independent physicians to certify in writing that your parent is mentally or physically incompetent. In a 2026 medical landscape of overwhelmed specialists and HIPAA-paranoid administrators, this can take weeks.

The Cost of the Gap: During those weeks, your parent’s accounts are locked. You cannot move money to pay for the $500-a-day nursing home bed, you cannot file insurance claims, and you cannot stop the automatic "vampire" drafts hitting their bank account.

The Forensic Upgrade: You need a Durable Power of Attorney that is active immediately upon signing. This grants you Attorney-in-Fact status today, allowing for a seamless transition of governance without a "medical waiting period" that bleeds the estate dry.

2. The "Specific Authority" Chokepoint

The system banks on the fact that your POA is likely a "General" document. In the world of Long-Term Care Financial Planning, "General" means "Incomplete."

The "Gifting" Trap: If your document does not contain a Specific Grant of Authority to make gifts or transfers, the law presumes you cannot do it. Why does this matter? Because Medicaid planning often requires moving assets to a spouse or a trust to meet eligibility requirements.

The Medicaid Blockade: If you try to move a deed or transfer cash to protect it from the state without this specific language, the County Clerk or the bank will reject the transaction. You are then stuck in a "Spend-Down" spiral, forced to liquidate every cent of your parent’s legacy to pay for care simply because your legal document lacked a single paragraph of code.

The Forensic Review: At 2nd Look Services, we sweep your documents for the "Super-Powers"—specific clauses for gifting, creating trusts, and managing digital assets—ensuring your authority is recognized by state Medicaid auditors.

3. The SSA Representative Payee Lockout

This is the most common "Ignorance Surcharge" for the Household CFO: The assumption that a POA works at the Social Security Administration.

It does not.

The Federal Wall: The SSA is a federal entity that flatly refuses to recognize state-level Power of Attorney documents. They do not care if you have a "Durable" status or an "Attorney-in-Fact" designation.

The Cash Flow Failure: If your parent’s check is diverted, stolen, or needs a change of address, the SSA will not talk to you. If the facility doesn't get paid because the check is in limbo, they will issue an eviction notice.

The Forensic Solution: You must be formally appointed as a Representative Payee through the SSA’s internal portal. This is a separate "Growth Engineering" step that must be done in tandem with your legal sweep to ensure the income stream—your primary cash flow for care—never stops.

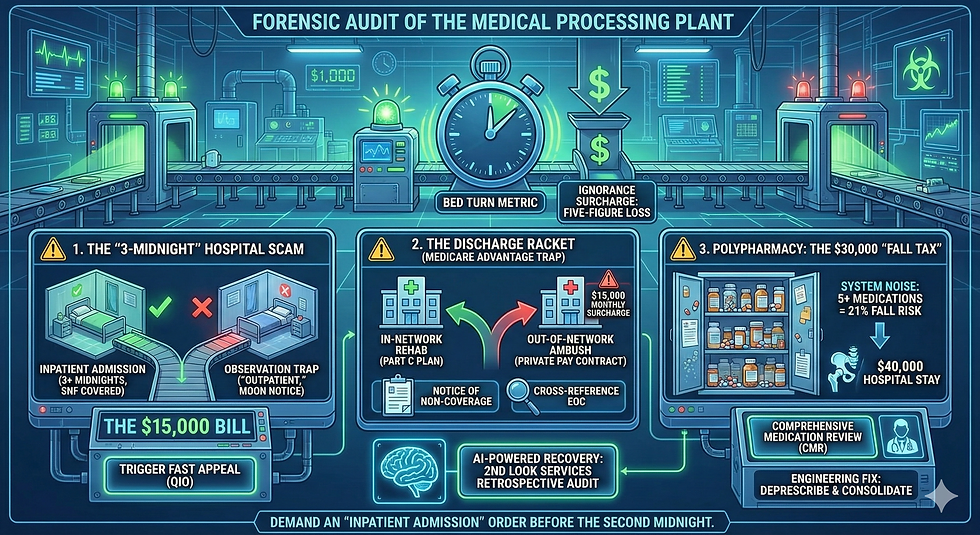

The Medical Pillar: Engineering the Care Triage

The medical system is not your ally; it is a high-volume processing plant designed for "Acute Care"—stabilizing a crisis and clearing the bed. As a Household CFO, you must realize that hospitals operate on a "Bed Turn" metric. If you aren't forensically auditing their billing codes in real-time, you are essentially volunteering for a five-figure Ignorance Surcharge.

1. The "3-Midnight" Hospital Scam: Observation vs. Admission

Medicare Part A only covers the astronomical cost of a Skilled Nursing Facility (SNF) if your parent was a formal "Inpatient" for at least three consecutive midnights.

The "Observation" Trap: Hospitals frequently classify seniors as being in "Observation Status." To you, it looks like a hospital room. To the doctor, it looks like care. But to the billing department, it is "Outpatient" care.

The $15,000 Bill: If your parent spends four days in a hospital bed under "Observation" and then moves to rehab, Medicare will pay $0 for that rehab. You will receive a MOON (Medicare Outpatient Observation Notice), which is effectively a legal warning that you are about to be hit with a private-pay bill averaging $500 per day.

The Forensic Play: You must demand an "Inpatient Admission" order before the second midnight. If the hospital refuses, you must trigger a Fast Appeal with the Quality Improvement Organization (QIO) immediately. At 2nd Look Services, our AI identifies these misclassifications retrospectively to recover funds you've already "lost" to this billing shell game.

2. The Discharge Racket: The Medicare Advantage Trap

Hospitals are financially penalized for "Long Stays." Their goal is to move your parent to the first available bed in the community.

The Out-of-Network Ambush: If your parent has a Medicare Advantage (Part C) plan, the hospital may "discharge" them to a facility that is not in that plan's specific network. Once you sign those admission papers at the rehab center, you have legally entered a private-pay contract.

The "Notice of Non-Coverage": You have the right to a "Detailed Notice of Discharge" that explains exactly why the hospital thinks care is no longer "medically necessary."

The CFO Strategy: Never accept the first facility on the social worker's list. You must cross-reference the facility with the Evidence of Coverage (EOC) for your parent's Part C plan. If the hospital pushes an out-of-network placement, they are effectively imposing a $15,000 monthly surcharge on your estate.

3. Polypharmacy: The $30,000 "Fall Tax"

A Household CFO understands that "System Noise" leads to failure. In medicine, this noise is called Polypharmacy—the dangerous accumulation of 5, 10, or 15 different medications prescribed by specialists who never talk to each other.

The Financial Death-Spiral: Taking 5+ medications increases the risk of a catastrophic fall by 21%. A fall leads to a hip fracture, which leads to a $40,000 hospital stay, which leads to permanent long-term care. This is the ultimate "Ignorance Surcharge."

Medication Therapy Management (MTM): If your parent is on 8+ Part D drugs and has 3+ chronic conditions, they are likely eligible for a Comprehensive Medication Review (CMR) at no cost.

The Engineering Fix: You must consolidate all scripts into one pharmacy. You are looking for an "MTM-certified" pharmacist to act as the "Human API," auditing the "drug-to-drug" interactions and "deprescribing" the toxic combinations that are quite literally bankrupting your family through medical instability.

The DIY Disaster: Why "Doing it Yourself" is Financial Suicide

You can choose to engineer this recovery yourself.

But as a Household CFO, you must weigh the ROI of your own time:

The DIY Investment: 150+ Hours of manual research, reading 50,000+ pages of state-specific Medicaid manuals and federal codes.

The Burn Rate: Every month you "wait and see" while navigating the red tape is another $15,000 drained from the estate.

The Personal Cost: You stop being a son or daughter. You become an unpaid, stressed-out paralegal and billing clerk for a system that wants you to fail.

2nd Look Services removes the burden. Our AI performs a Forensic Review of every law, court case, and obscure county code to find the money the system is trying to hide. We don't guess. We engineer a recovery.

Stop the Legacy Liquidation Trap. Reclaim Your Legacy.

The "Ignorance Surcharge" ends today.

The system is betting on your silence and your exhaustion. Don’t prove them right.

Take the first step toward a Forensic Sweep and protect what your family has earned. As a Household CFO watching an inheritance vanish, you need a Financial Equalizer. Do not fall into the Legacy Liquidation Trap.

Contact Don Zavis at +1 (248) 497-5869 now to initiate your professional Forensic Review. Let’s look at the numbers, look at the laws, and recover what’s yours.

Earn it. Return it. Retain it.

Comments